People wearing face masks walk at a main shopping area, following the coronavirus disease (COVID-19) outbreak in Shanghai, China January 27, 2021. REUTERS/Aly Song/File Photo

A look at the day ahead from Saikat Chatterjee.

China's disappointing monthly activity data suggests the world's No.2 economy is losing steam more quickly than anticipated and sets the scene for a cautious start to the week.

July retail sales, industrial production and fixed asset investment were all weaker than expected as the latest COVID-19 outbreak weighs. Investors hoping for more stimulus may have to wait longer as Beijing policymakers want to allow July's reserve requirement ratio cut to take effect before taking further action. read more

Nevertheless, the weak data has stalled the upward march of global stocks and pulled Asian shares towards last month’s lows. European and U.S. stock futures suggest a cautious start to the week.

Add Friday's news of a shock slump in U.S consumer sentiment to the lowest since 2011 and bond markets are back on a tear.

U.S. 10-year Treasury yields are down 11 bps in the last two sessions as their prices rise, with geopolitical uncertainty after the collapse of the Afghan government supporting safe-haven assets. read more

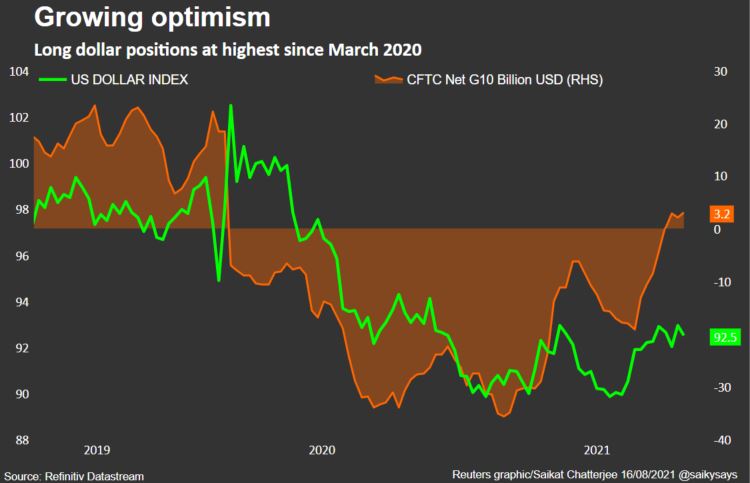

While the weak U.S. sentiment readings wiped off a week’s gain for the dollar against its major rivals, positioning data suggests more upside for the greenback.

Long dollar bets have grown to their biggest since March 2020. Minutes of the Federal Reserve's last policy meeting due this week will likely provide more fodder for dollar bulls, especially if more policymakers signal a likely tapering soon.

That central banks are moving to exit emergency stimulus should be clear this week, with New Zealand expected to become the first major economy to lift interest rates.

Money markets have priced in a full quarter point rate hike on Wednesday and a 25% probability of a 50 bps hike. Norway’s central bank could also signal the timing of its own rate rise possibly in autumn.

Earnings season meanwhile winds down with some impressive readings: European shares are reporting a 150% year on year earnings growth and U.S. stocks indicate a 90% earnings growth.

Key developments that should provide more direction to markets on Monday:

- Auctions: US 6-mth and 3-mth T-bills, US data on foreign buying of Treasuries in June.

- HSBC to buy Axa's Singapore insurance assets for $575 million. read more

- U.K. home asking prices slip for first time this year - Rightmove. read more

Reporting by Saikat Chatterjee; Editing by Dhara Ranasinghe

Our Standards: The Thomson Reuters Trust Principles.

"heavy" - Google News

August 16, 2021 at 02:05PM

https://ift.tt/3CQZdZW

MARKETMIND A heavy dose of caution - Reuters

"heavy" - Google News

https://ift.tt/35FbxvS

https://ift.tt/3c3RoCk

heavy

Bagikan Berita Ini

Related Posts :

Heavy lake effect snow in Buffalo forecast for Dolphins-Bills - NBC Sports

Heavy lake effect snow in Buffalo forecast for Dolphins-Bills - NBC Sports- Report: Heavy Metals Found in Dozens of Dark Chocolate Brands - Entrepreneur

- Toxic heavy metals found in many chocolate bars including Hershey's, Ghirardelli - New York Post

- Heavy snow to bombard millions in Northeast this weekend as South recovers from deadly tornadoes - CNN

- Heavy metals found in dark chocolate including Hershey's and Trader Joe's - CBS News

0 Response to "MARKETMIND A heavy dose of caution - Reuters"

Post a Comment